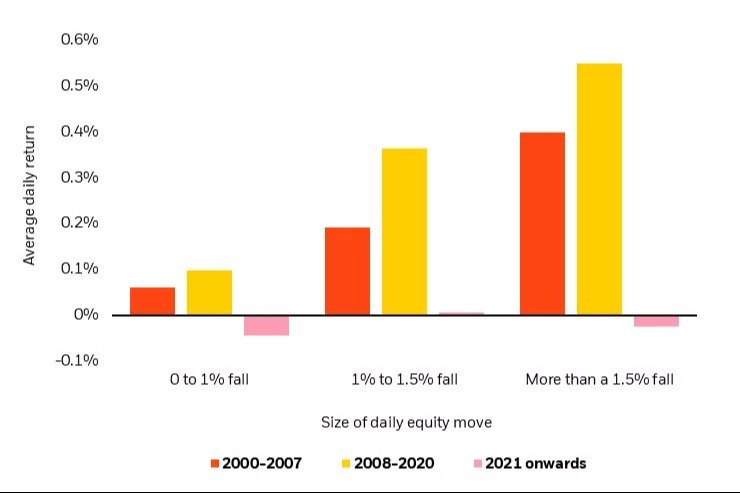

Sources: BlackRock Investment Institute, with data from Refinitiv Datastream, April 2023. Notes: The chart shows the average daily return of 10-year U.S. Treasuries on days when equity prices fell, based on the size of the drop in equity prices. The red bars show daily returns for the period 2000-2007, the yellow bars for the period 2008-2020 and the pink bars for 2021 onwards. All periods start in January and end in December for each respective range. The index used for equities is MSCI World.

Should you upgrade your investment strategy?

- Are you over the age of 50?

- Do you have over $1,000,000 of investable assets?

- Are you concerned about what a recession will do to your life savings?

Investing in alternatives is not a fit for everyone, but if you answered yes to all three questions above, they may be right for your portfolio.

Want to learn more?

Schedule an introduction to alternatives below.